1099 Workers: Claim Up to $32,220 in COVID Tax Credits (Deadline Alert!)

The Self-Employment Tax Credit (SETC) presents a significant financial opportunity for self-employed professionals, including freelancers, gig workers, and 1099 contractors, offering potential recovery from COVID-related income loss.. We're talking up to $32,220 back, but the deadline is looming.

Let's strategize how to claim it:

*you can file for this return with no fees, on your own too! Scroll to the bottom for directions, if you'd like to file on your own :)

- Opportunity:

- Up to $32,220 in tax credits.

- Covers 2021 income loss.

- Deadline: April 15, 2025 (Oct. 15 with extension).

Why SETC Tax Return? As your consultant, I’ve vetted them. They streamline the complex process and maximize your return, quickly. Here’s how:

- Features:

- Expert SETC recovery.

- Fast 5-7 day express refund option.

- Zero risk: no refund, no fee.

- Simple process, no document uploads.

- IRS approved firm.

- Benefit: Optimized financial strategy with minimal risk and maximum efficiency.

Quick Breakdown of Eligibility: Is this for you? As a consultant, I see this applying to many of my clients. If you're self-employed, an independent contractor, or a gig worker, you likely qualify. Here are some examples:

- Features:

- Covers business owners, delivery drivers, consultants, creatives, IT, healthcare, and more.

- Essentially anyone that filed a 1099.

- Benefit: Expanding your financial strategy to include all applicable credits.

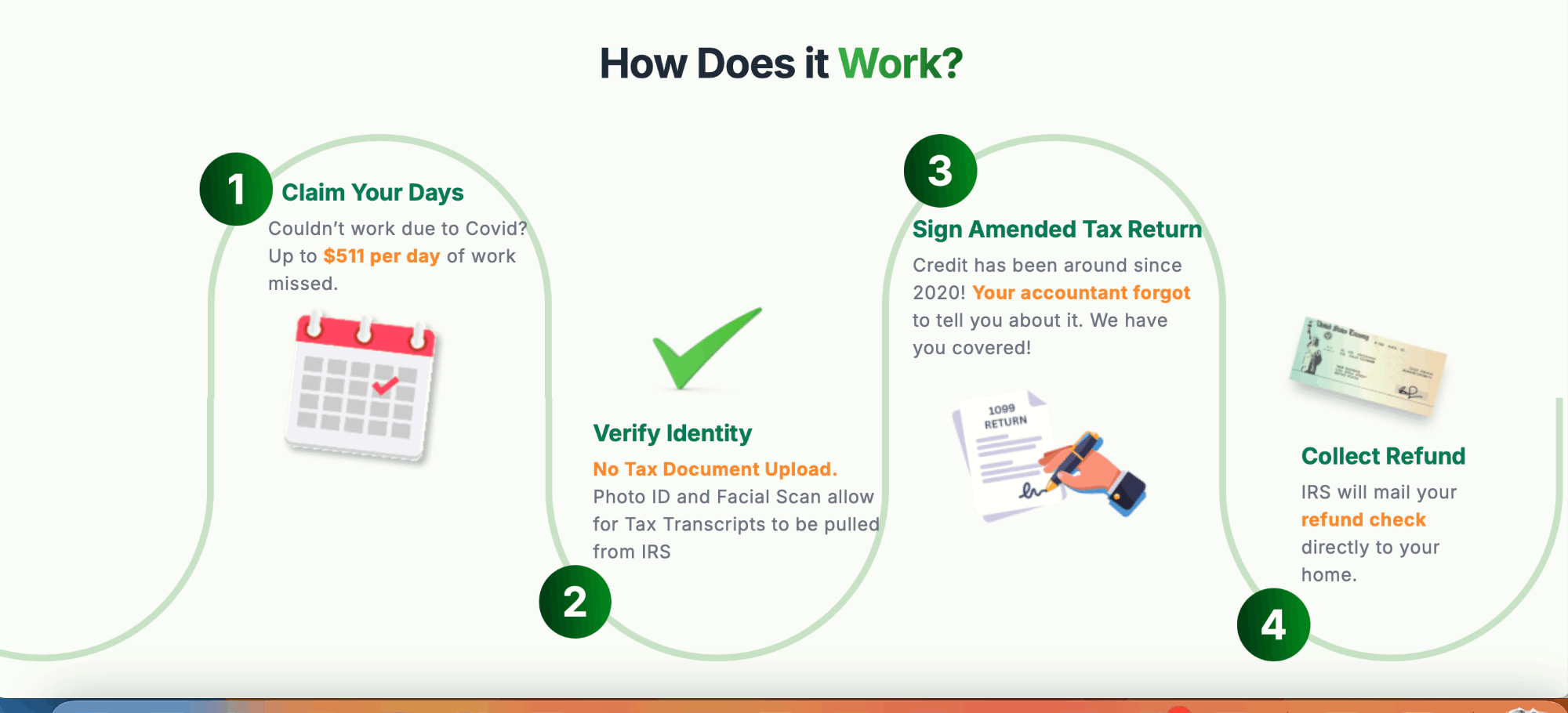

Credit Details: How it strategically works. The credit is calculated based on days you couldn't work due to COVID-related reasons, like personal illness or caring for a child.

- Features:

- Up to $5,110 for personal sick days.

- Up to $12,000 for caregiving.

- SETC Tax Return's software handles all calculations.

- Benefit: Strategic maximization of available funds with precise calculations.

Payment Options: Flexible financial planning. We offer multiple payment options to fit your strategic financial needs:

- Fee Options:

- Express Refund: 30% upfront, 5-7 day refund.

- Standard Refund: 15% upfront, IRS processing time.

- Deferred Payment: 20% after refund receipt.

Let’s strategize this win. Time is ticking. Any questions on how this fits into your overall business strategy?

Who Qualifies?

- Business Owners: Any self-owned business (retail, manufacturing, service-based, etc.).

- Independent Contractors, Freelancers, and Gig Workers:

- Delivery Services: DoorDash, Uber Eats, Amazon Flex, etc.

- Construction: Carpenters, electricians, plumbers, etc.

- Ridesharing/Transportation: Uber, Lyft, taxi drivers.

- Consulting: Management, IT, marketing, financial consultants.

- Event Planning: Coordinators, wedding planners.

- Creative Arts: Artists, musicians, performers.

- Information Technology (IT): Software developers, web designers.

- Healthcare: Traveling nurses, therapists, independent physicians.

- Freelance Writing/Editing: Content creators, editors, proofreaders.

- Personal Services: Hairstylists, personal trainers, massage therapists.

- Anyone who received a 1099 form for work provided.

FAQs

Q: What is the Family First Coronavirus Response Act (FFCRA)?

A: The Family First Coronavirus Response Act (FFCRA) is a United States federal law enacted in March 2020 in response to the COVID-19 pandemic. It aimed to provide emergency paid sick leave, expanded family and medical leave, and enhanced unemployment benefits to individuals affected by the pandemic. The FFCRA required certain employers to provide employees with paid sick leave or expanded family and medical leave for specified reasons related to COVID-19. Additionally, it provided tax credits to help employers offset the costs of providing these benefits. The FFCRA had various provisions that applied to different types of employers and employees, with the goal of supporting workers and their families during the public health emergency caused by the coronavirus outbreak.

In December 2020, under the CARES Act, self employed individuals were included to receive tax credit for sick and family leave.

Q: What is the CARES Act?

A: The Coronavirus Aid, Relief, and Economic Security (CARES) Act is a significant piece of legislation enacted by the United States Congress in March 2020 in response to the economic impact of the COVID-19 pandemic. The CARES Act aimed to provide financial relief to individuals, businesses, and healthcare systems affected by the pandemic. Some key provisions of the CARES Act include:

-

1. Economic Impact Payments: The CARES Act authorized direct payments to individuals and families to help alleviate financial strain caused by the pandemic. These payments, also known as stimulus checks, were sent to eligible taxpayers based on their income and filing status.

-

2. Small Business Assistance: The CARES Act established the Paycheck Protection Program (PPP) to provide forgivable loans to small businesses to cover payroll costs, rent, mortgage interest, and utilities. It also expanded the Economic Injury Disaster Loan (EIDL) program and provided grants to eligible businesses.

-

3. Unemployment Benefits: The CARES Act expanded unemployment insurance benefits by providing additional federal funding, extending benefits to self-employed individuals and gig workers, and increasing the duration of benefits.

-

4. Healthcare Funding: The CARES Act allocated funding to support healthcare providers, hospitals, and medical research efforts in combating the COVID-19 pandemic. It also included provisions to expand access to telehealth services.

-

5. Education and Housing Assistance: The CARES Act provided funding for K-12 schools, colleges, and universities to support distance learning and address other pandemic-related challenges. It also included measures to provide housing assistance and prevent evictions and foreclosures.

Overall, the CARES Act was intended to provide immediate economic relief and support to individuals, businesses, and communities affected by the unprecedented challenges posed by the COVID-19 pandemic.

Q: What is the Self-Employed Tax Credit (SETC)?

A: The self-employed tax credit was created under the Family First Coronavirus Response Act (FFCRA) and extended by the American Rescue Plan Act (ARP). It is a financial aid program for self-employed individuals, freelancers, and independent contractors. This credit aims to compensate those who experienced a loss of income due to COVID-19 related reasons.

Q: Is the credit a loan, grant, or taxable?

A: No, this credit is not a loan or a grant, nor is it taxable. Unlike loans, there's no requirement to repay this tax credit. Additionally, it is not considered as taxable income.

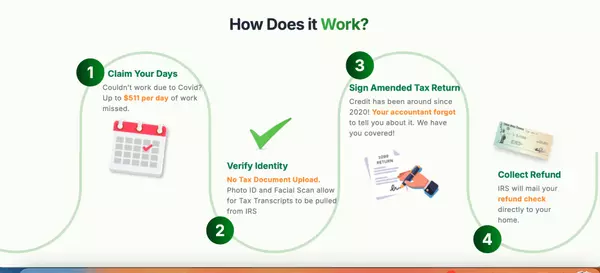

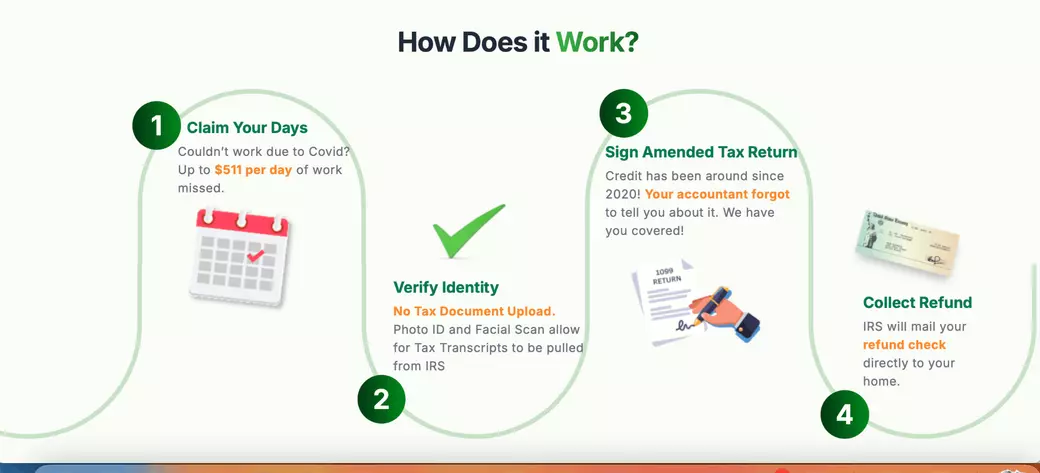

Q: How to I submit my amended documents?

A: After downloading and executing all documents the applicant will send them to SETC Tax Return via UPS. A QR code is provided that will be used at UPS to receive a prepaid and pre-labeled envelope. Place all the documents inside the envelope and send it off.

Q: How long does it take to receive my credit?

A: The processing time with the IRS can vary, typically ranging between 16 to 24 weeks from the time of your application submission to receiving your refund check.

Q: If I owe back taxes, will I still receive the full credit amount?

A: If you owe back taxes, the IRS will apply any credit you are eligible for against your outstanding tax liabilities first, before you are directly compensated. This means the full amount of the credit may be used to reduce or eliminate your back taxes owed. If the credit exceeds the amount you owe, you will receive the remaining balance as a refund.

Q: What is the IRS Form for the SETC tax credit?

A: In order to calculate and claim your return, you will need to submit the IRS form 7202, “Credits for Sick Leave and Family Leave for Certain Self-Employed Individuals”. Our software will automatically generate form 7202 once you complete the questionnaire and we pull your tax transcripts from the IRS.

Q: What defines a self-employed individual for the SETC program?

A: For the SETC program, a self-employed individual is defined as someone who earns income directly from their own business, trade, or profession, rather than as an employee of another company. This includes freelancers, independent contractors, sole proprietors, and members of partnerships. To be considered self employed for this credit you will also need to have a schedule C and or schedule SE in your tax returns.

Q: What are some examples of qualifying work?

A: Some examples of self-employed work that would qualify you for the self-employed tax credit are:

-

1. Business owner: Product, trade, or any other service performed under your own business.

-

2. Independent Contract, Freelance, or Gig work: Some examples include, but are not limited to:

a. Delivery Services: Independent contractors may work for delivery companies like DoorDash, Grubhub, Uber Eats, FedEx, UPS, or Amazon Flex, delivering packages or food orders.

b. Construction: Independent contractors in construction may include carpenters, electricians, plumbers, painters, and general contractors who are hired to complete specific projects or tasks.

c. Ridesharing and Transportation: Drivers for companies like Uber, Lyft, or taxi services operate as independent contractors, providing transportation services to passengers.

d. Consulting: Independent contractors in consulting offer their expertise and services in various fields such as management consulting, IT consulting, marketing consulting, or financial consulting.

e. Event Planning: Independent contractors in event planning may include event coordinators, wedding planners, or corporate event organizers who are hired to plan and execute events for clients.

f. Creative Arts: Artists, musicians, actors, and performers often work as independent contractors, taking on freelance gigs or projects such as exhibitions, performances, or commissioned work.

g. Information Technology (IT): Independent contractors in IT may work as software developers, web designers, IT consultants, or cybersecurity experts, providing services to businesses on a contract basis.

h. Healthcare: Independent contractors in healthcare include physicians, traveling nurses, therapists, or medical specialists who provide temporary or specialized services to healthcare facilities.

i. Freelance Writing and Editing: Writers, editors, and journalists often work as independent contractors, providing content creation, editing, or proofreading services to clients.

j. Personal Services: Independent contractors in personal services may include hairstylists, personal trainers, massage therapists, or private tutors who offer their services on a freelance basis.

Q: Can I use my 2020 income if it was larger than my 2021 income?

A: Yes, you can use your previous years net income if it was higher. For 2021, you may use your 2020 net income if it was larger than 2021.

Q: Can I receive the tax credit if I was a W2 employee and self-employed?

A: Yes, if you were both a W2 employee and self-employed, you can still qualify for the tax credit, as long as your self-employed work meets the SETC program's eligibility criteria. However, if you already claimed your full sick and family leave as a W2 employee, you may not be eligible to receive more.

Q: If I filed jointly, can my spouse and I both receive the credit?

A: Yes, if you and your spouse both qualify as self-employed and filed taxes jointly, you're each eligible to claim the credit. However, you must create an account together as you will both be able to claim days under one account. DO NOT create separate accounts.

Q: Can I count weekends as missed work days?

A: Yes, you can count weekends as missed work days for the credit if those days are typical working days for your self-employment activities and you were unable to work due to COVID-19 related reasons.

Q: Does applying for the SETC credit affect my credit score?

A: No this will not affect your credit score! Our process does not include any credit inquiries.

Q: What documentation is required to apply?

A: There's no need for you to upload any documents manually! To apply, you simply need to complete our questionnaire, verify your identity, and authorize us to access your tax information. We'll then electronically retrieve your tax returns from the IRS and calculate your exact refund amount.

Q: I was married filed jointly in 2021 but am divorced now. What should I do?

A: Yes, if you filed as Married Filing Jointly (MFJ) in 2021, both you and your former spouse must sign the current 1040 and 1040X forms for the SETC refund, even if you are now divorced or separated. If your former spouse is deceased, you may need to include a copy of their death certificate when mailing the final documents to the IRS.

Q: Why is the Routing & Account # on the form 8888 not my account info?

A: Form 8888 tells the IRS where to deposit your refund. For clients using Chase Bank or PNC Bank, after entering your routing and account number on Form 8888 and printing it, the form will not display your actual account information. Instead, it will show a "tokenized" routing and account number.

Independent Filing for the Self-Employment Tax Credit (SETC): Process Overview

*This information is provided for informational purposes only and should not be considered professional tax advice. Consult with a qualified tax professional for personalized guidance or explore the services mentioned above for expert assistance.

Individuals who choose to independently file for the Self-Employment Tax Credit (SETC) must adhere to specific IRS guidelines. This process requires the completion and submission of Form 7202, which is used to calculate the credit based on income lost due to COVID-19 related circumstances.

The calculation of the SETC involves several factors, including net self-employment income and the number of days the individual was unable to work due to COVID-19.

- Personal Illness: For days unable to work due to personal illness or quarantine, the credit is up to $511 per day, with a maximum of 10 days, or $5,110.

- Caregiving: For days spent caring for a family member with COVID-19 or a child whose school or daycare was closed, the credit is two-thirds of the average daily net self-employment income, up to $200 per day. For the 2021 tax year, this applies to a maximum of 60 days, or $12,000.

- Average Daily Income: The average daily net self-employment income is calculated by dividing annual net self-employment income by 260.

Independent filing requires careful attention to detail and knowledge of IRS regulations. Individuals may seek assistance from tax professionals, who typically charge a fee for their services.

Categories

Recent Posts